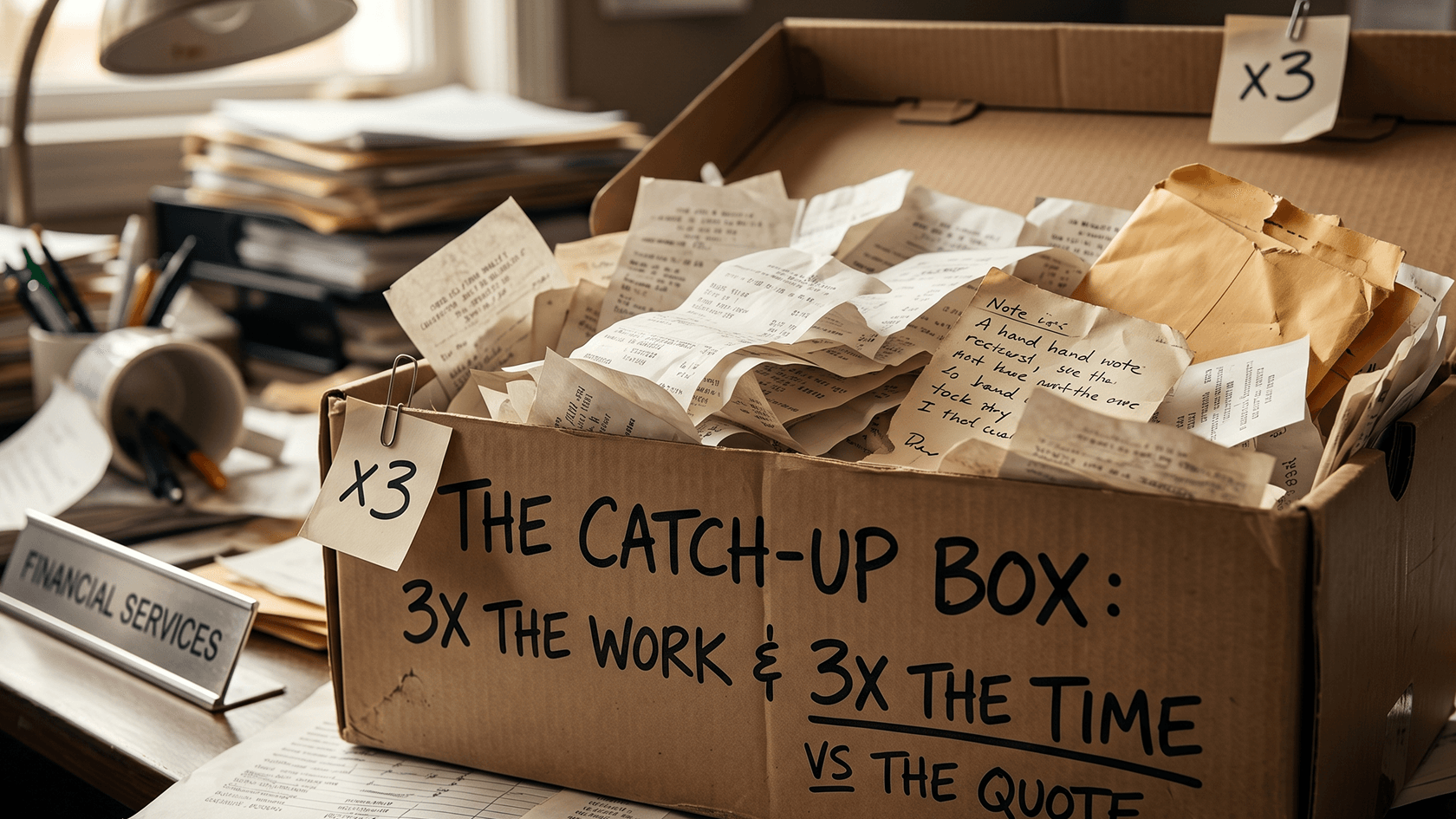

Why the Quote Is Almost Always Wrong

The estimate for a catch-up job is usually built on one number: how many months are behind. Three months behind, quote three months of work. Six months, double it. That logic sounds fair until you start and realise the months aren't the problem. The problem is what's inside them.

Missing source documents are the first thing that adds time. Bank statements with gaps, invoices that were never received, receipts the client swears exist but can't locate, none of that shows up during the initial scoping call. It only surfaces once you're already in the file trying to reconcile a transaction that has no paper trail behind it. Every gap becomes a conversation, then a chase, then a delay. And that's before you've touched a single GST code.

The second thing that kills estimates is compounding. A bank rule that was miscoding transactions twelve months ago didn't just create one error. It created the same error every time that transaction type appeared, across every period since. Fixing it means going back and correcting each instance individually, then checking whether those corrections ripple into BAS periods that have already been lodged. A single bad rule from eighteen months ago can turn a three-hour fix into a full day. None of that is visible from the outside when you're building a quote.

Where the Hidden Hours Actually Live

The biggest time sink in catch-up work isn't the volume of transactions. It's the decisions that have to be made about unclear ones. Every transaction that could be coded two ways requires a judgment call, and judgment calls slow everything down. Mixed-use expenses, personal transactions sitting in the business account, payments to related parties with no description, each one needs to be investigated, not just categorised.

GST errors that ripple forward are the other major source of blowout that rarely gets priced in. If a client was on the cash basis but their bookkeeper was coding accrual-style, or if input tax credits were claimed on GST-free purchases across multiple quarters, correcting the current period isn't enough. You need to work out which past BAS periods are affected, whether amendments are required, and whether the corrections change anything that's already been lodged with the ATO. That work can't be estimated from the outside. It depends entirely on what you find once you're in.

The pattern that causes most of the damage is simple: firms quote based on what the client tells them, then price the hours required to do clean work on clean data. Catch-up data is never clean. The quote should include time to assess what's actually there before pricing the work to fix it.

The Takeaway

Catch-up bookkeeping blows out because the estimate is built on assumptions that the data inside the job will prove wrong. The months behind is the starting point, not the scope. A scoping process that works needs to include a paid or fixed-fee assessment phase before a full quote is given, enough time to look at the actual file, identify missing documents, spot recurring bank rule errors, and check whether past BAS periods have been affected by whatever coding decisions were made along the way. Firms that build assessment into the process quote more accurately, manage client expectations better, and stop absorbing the cost of hours they didn't price for.