This hesitation isn’t resistance to technology

When accountants pause before enabling AI-driven categorisation or automation inside the ledger, it’s often framed as conservatism or resistance to change. That framing is wrong. Most experienced accountants are not afraid of automation. They are afraid of misplaced certainty. The ledger is not just a tool. It is the historical record that underpins BAS, audits, and professional liability. Once something is written into it, the cost of being wrong rises sharply.

The ledger is not where experimentation belongs

AI works by making probabilistic decisions. That is its strength. It recognises patterns, fills gaps, and acts quickly when information is incomplete. Inside the ledger, those same strengths become risks. When an AI misclassifies a transaction directly into the accounting file, the error is no longer hypothetical. It becomes part of the financial history. Correcting it later requires detection, context, and time — all of which are scarce during BAS. This is why senior accountants instinctively hesitate. Not because they distrust AI, but because they understand the consequences of committing decisions too early.

Why rules-based automation feels safer than it is

Traditional bank rules feel predictable. They are explicit. If a description matches, a rule fires. If it doesn’t, nothing happens. That predictability creates a sense of control, even when the underlying logic is fragile. AI introduces a different dynamic. Decisions are made based on interpretation, not strict matching. For business owners, that feels magical. For accountants, it feels opaque. The concern is not that AI will always be wrong. It’s that when it is wrong, the reasoning is invisible, and the correction happens too late.

The unspoken fear: contaminating the source of truth

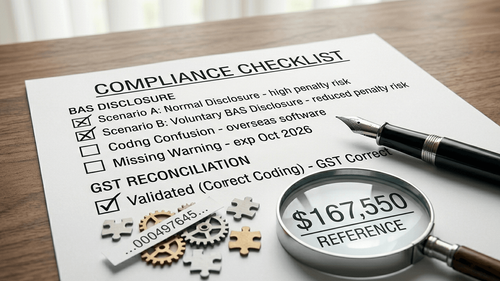

Ask any senior accountant what they protect most fiercely, and the answer is rarely speed. It is integrity. Once the ledger is contaminated, every downstream report inherits that uncertainty. Reconciliation may still balance. BAS may still lodge. But confidence erodes. This is why many accountants prefer manual review, even when it is slower. It preserves trust in the file. That instinct is not outdated. It is professional judgement.

Review-first workflows mirror how accountants actually think

In practice, accountants do not make decisions in isolation. They review patterns, scan for anomalies, apply judgement in context, and only then commit entries. Review-first workflows respect that reality. They allow AI to assist without forcing premature commitment. Decisions are surfaced, grouped, reviewed, and verified before touching the ledger. This is not about reducing automation. It is about placing it where it supports accountability instead of undermining it.

Why this matters most before BAS

Before BAS, tolerance for uncertainty drops. Every assumption carries weight. The closer lodgement gets, the more accountants rely on files they trust, not systems they hope are correct. AI that operates directly inside the ledger increases speed, but it also increases the cost of being wrong. That trade-off is why many accountants hesitate. And why that hesitation should be taken seriously.

The takeaway

Accountants don’t distrust AI because they fear technology. They distrust AI inside the ledger because they understand responsibility. Trust is not built by hiding uncertainty. It is built by creating space to review it.