How the ATO Sets the Penalty

When a BAS contains an error that results in a tax shortfall, the ATO applies a penalty based on the behaviour that caused it. Failure to take reasonable care attracts a base penalty of 25% of the shortfall. Recklessness brings it to 50%. Intentional disregard of the law sits at 75%. These percentages apply to the shortfall amount itself, not to the total tax paid, so a $20,000 GST shortfall attributed to recklessness generates a $10,000 penalty before any reductions are applied.

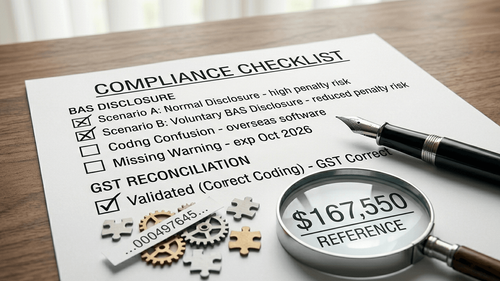

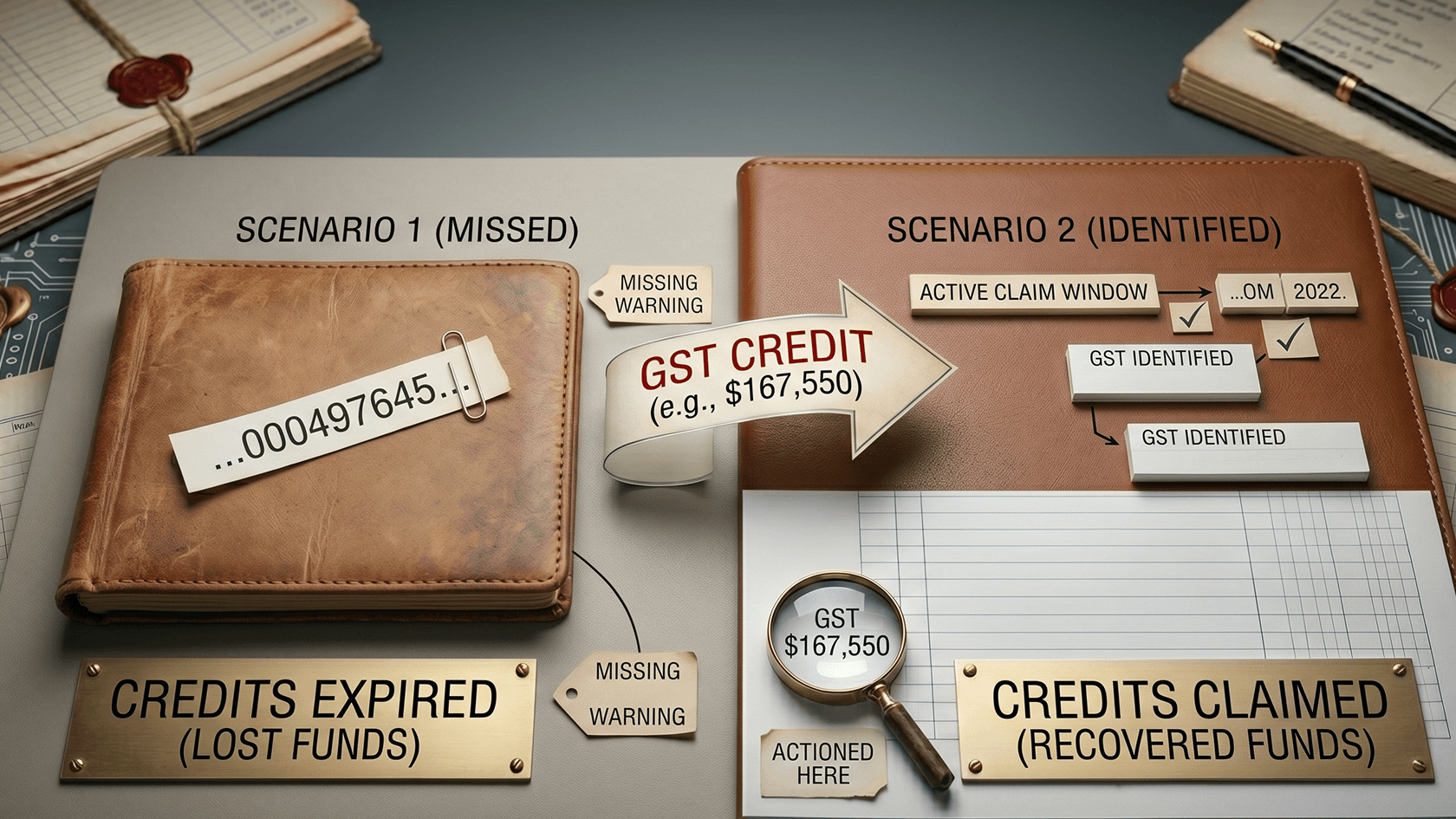

The key variable is when the error is disclosed. A voluntary disclosure made before the ATO notifies the entity of a review or audit can reduce the base penalty by up to 80%. The same disclosure made after the ATO has already initiated contact can still reduce it, but only by around 20%. Where the disclosed shortfall is under $1,000, the ATO can reduce the penalty to nil entirely.

The ATO also distinguishes between errors caused by the client and errors caused by the firm. A client is not liable for a false or misleading statement penalty if the error was caused by the registered tax agent or BAS agent failing to take reasonable care, provided the client gave the agent all relevant information. That safe harbour does not protect the firm.

What Counts as a Voluntary Disclosure and How to Make One

A voluntary disclosure has to be made in the approved form and has to genuinely notify the ATO of the shortfall or the false or misleading nature of the original statement. Sending an amended BAS through the accounting software is the most common method for GST corrections. For corrections made outside a review or audit, the client can also lodge through ATO Online Services for Business or in writing via secure mail.

The disclosure does not require an admission of liability. The ATO's published guidance confirms that a client does not need to admit they were wrong when making a voluntary disclosure, only that there is a correction to be made. What matters is that the shortfall is identified clearly, the relevant period is specified, and the facts are provided in enough detail for the ATO to assess it without needing to conduct further examination.

Timing is everything here. Once the ATO has issued a notice of review or audit for the relevant period, the 80% reduction is no longer available. Firms that discover an error in a client file and wait to see whether the ATO notices are taking a risk that sits with the client but reflects directly on the firm.

The Takeaway

A BAS error found after lodgement is fixable. A BAS error found by the ATO first is significantly more expensive. The voluntary disclosure framework exists precisely to create an incentive for early correction, and the penalty reduction for acting before ATO contact is substantial enough that the cost of not disclosing almost always exceeds the cost of disclosing. When an error is found, the right move is to quantify the shortfall, prepare the amended BAS or written disclosure, and lodge it before the ATO has any reason to be looking at that period. The firm's job is to make sure the client understands that clearly, and to move quickly once the decision is made.