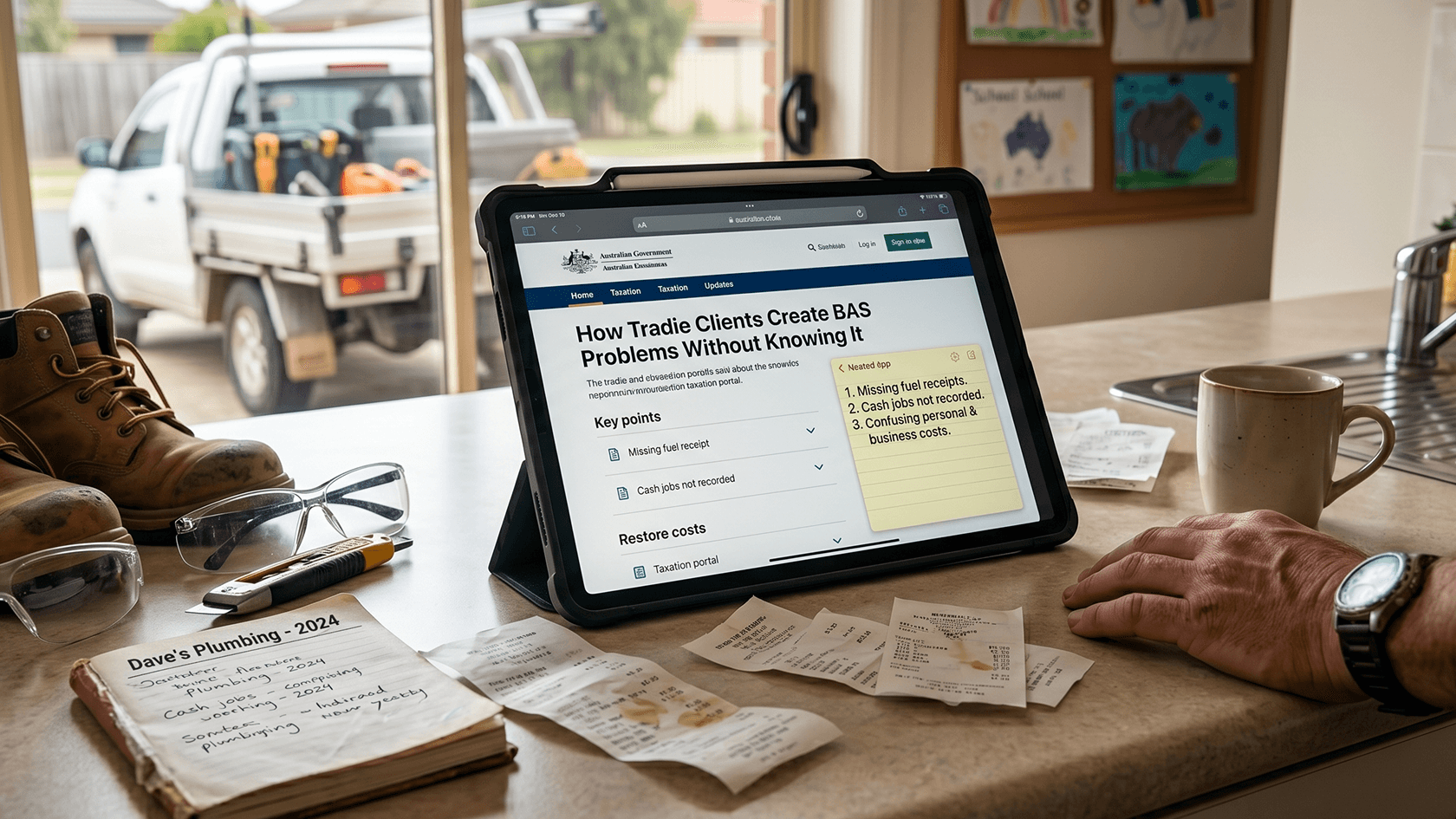

Why Tradies Create More BAS Work Than Most Clients

It's not deliberate. A plumber running three jobs a day, quoting on a fourth, and ordering materials on the weekend isn't thinking about GST coding when they swipe their card. But by the time the quarter closes and the BAS needs to go in, the file tells a different story. Personal purchases mixed into the business account. Tools bought under a chattel mortgage where the GST was claimed upfront on the BAS but the asset wasn't added to the register. Cash income that came in through a mate's account and never made it into the books at all.

The six errors that come up most consistently with tradie clients are: mixing personal and business accounts, failing to charge GST once turnover crosses the $75,000 threshold, claiming GST on wages and super (which carry no GST), incorrect treatment of plant and equipment purchased under finance, not recording cash income, and applying the wrong business-use percentage to vehicles used for both work and personal purposes. None of them are exotic. Every one of them is avoidable with the right setup and a bit of work at onboarding.

The vehicle issue is worth specific attention. Commercial vehicles with a load capacity over one tonne are not subject to the car limit and can be written off in full under the instant asset write-off if they cost less than $20,000 and are used before 30 June 2026. But when the vehicle is used for both work and personal trips and no logbook exists, the business-use percentage the client gives you is usually a guess. Claiming a write-off on a vehicle with no logbook and a vague percentage is a defensibility problem waiting to surface.

Where Things Go Wrong at Quarter End

The threshold issue catches more tradies than it should. GST registration is compulsory once annual turnover hits $75,000, and the obligation to charge GST kicks in from the date registration is required not the date the client gets around to registering. A tradie who crosses the threshold in March but doesn't register until June has been undercharging GST for three months. The GST liability still exists. It just comes out of their margin instead of being collected from the client.

Equipment purchased under chattel mortgage adds another layer. For GST-registered businesses, the full GST credit on the purchase price can be claimed on the next BAS, but the deduction for income tax purposes is calculated on the GST-exclusive cost. When the bookkeeper codes the asset at the wrong value, or the GST credit gets claimed twice, once through the BAS and once as part of the write-off calculation, you end up with an error that spans two separate obligations and takes longer to untangle than either one on its own.

Cash income is harder to verify but worth asking about at every quarterly review. Tradies who do cash jobs, especially small residential work, sometimes don't record it because it doesn't go through the business account. That income is still taxable and still affects the GST turnover figure. If the bank feed looks inconsistent with the volume of work the client describes, it's a reasonable prompt to ask the question.

The Takeaway

Tradie clients don't create BAS problems on purpose. They create them because their work is physical, fast, and mostly done by people who aren't thinking about tax codes while they're on the tools. The fix is to do the heavy lifting at onboarding: separate accounts, a clear process for receipts and invoices, a logbook for any vehicles with mixed use, and a quarterly check on turnover relative to the GST threshold. Firms that build a tradie-specific review into their quarterly workflow catch these errors before they compound, rather than spending time untangling them at BAS lodgement.