What the Rules Actually Say

The $20,000 instant asset write-off is available to businesses with aggregated turnover under $10 million that use the simplified depreciation rules. It applies per eligible asset first used or installed ready for use for a taxable business purpose between 1 July 2025 and 30 June 2026. Both new and second-hand assets qualify. Without further legislation, the threshold reverts to $1,000 from 1 July 2026, which makes the current window genuinely time-sensitive for clients with planned purchases.

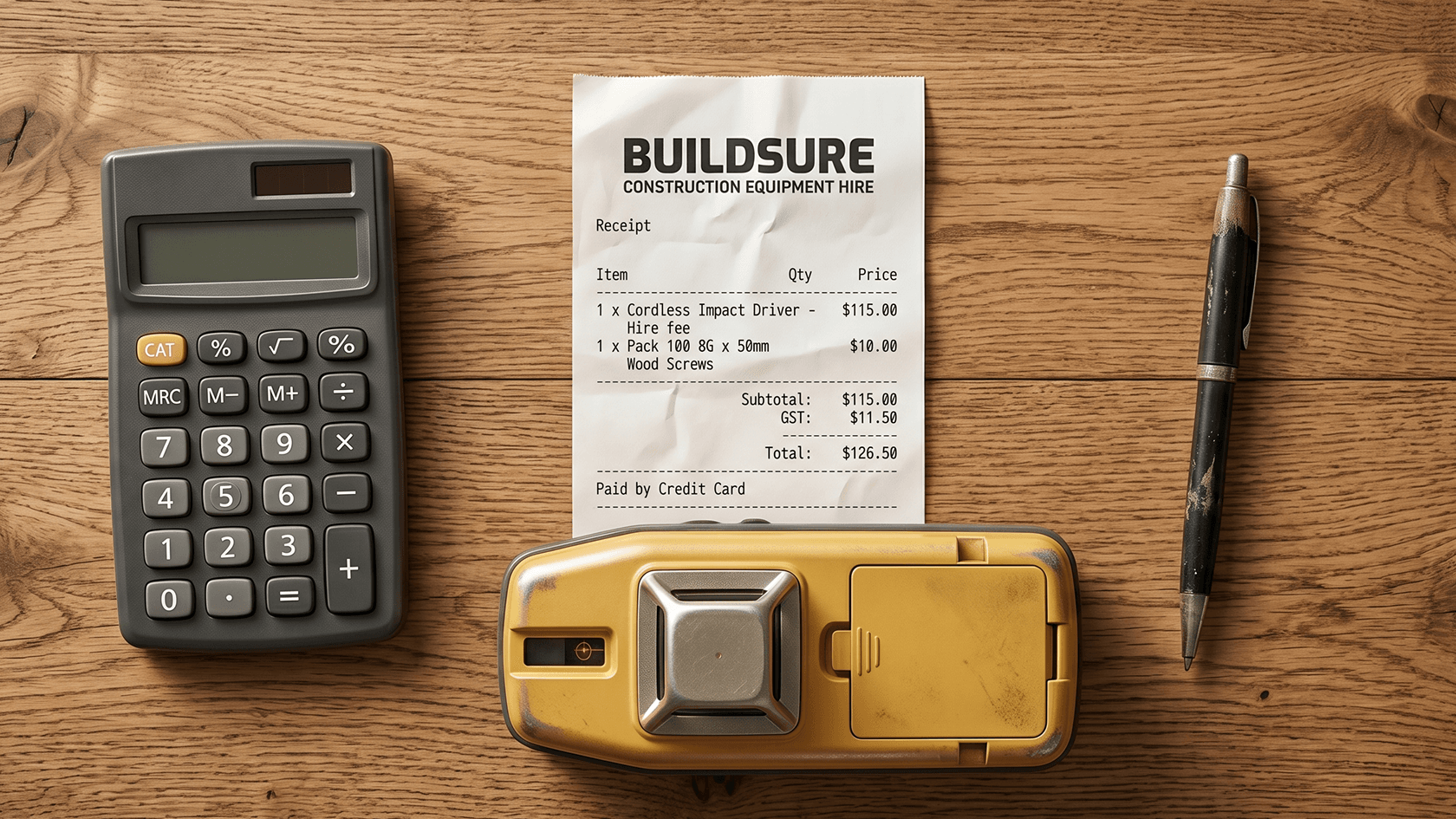

The $20,000 threshold is GST-exclusive for registered businesses. A client who is registered for GST and buys a $19,800 GST-inclusive asset is actually buying a $18,000 asset for write-off purposes, with $1,800 claimed separately as an input tax credit on the BAS. A client who is not registered for GST uses the full GST-inclusive price. Getting this wrong in either direction either inflates the deduction claimed or incorrectly excludes an asset that would have qualified once the GST is stripped out.

The threshold applies to the full cost of the asset, not to the deductible portion. If a client buys a $21,000 piece of equipment and uses it 80% for business, the write-off does not apply even though the deductible amount would be $16,800. The total cost exceeds the limit, so the asset goes into the small business pool and is depreciated at 15% in the first year and 30% thereafter.

Where the Coding Errors Happen

Vehicles cause the most problems. Passenger vehicles, defined as those designed to carry fewer than nine passengers with a load capacity under one tonne, are subject to the car limit, which is $69,674 for 2025-26. A client buying a $75,000 SUV used 100% for business cannot write off $75,000 or even $69,674. The car limit caps the depreciable value at $69,674, and because the purchase price exceeds $20,000, the instant asset write-off does not apply at all. The asset goes into the depreciation pool. Commercial vehicles with a payload over one tonne, such as most tradies' utes and vans, are not subject to the car limit and can be written off in full if the cost is under $20,000.

The second consistent error is treating the purchase date as the qualifying event rather than the use date. An asset ordered in June 2026 but delivered and installed in July 2026 does not qualify for 2025-26. The ATO's rule is clear: the asset must be first used or installed ready for use within the income year. For equipment requiring shipping, commissioning, or installation, that distinction matters and clients buying in May or June are at real risk of missing the window if delivery is delayed.

Third, the income tax write-off and the GST credit are two separate things. The write-off is claimed in the income tax return, calculated on the GST-exclusive cost. The GST credit is claimed on the BAS for the period the purchase was made. Firms that fold the GST into the write-off calculation, or that code the full GST-inclusive amount as the deductible figure, create an error that spans both the BAS and the tax return.

The Takeaway

Before processing any instant asset write-off claim, four questions need answers: Is the business's aggregated turnover under $10 million and are they using simplified depreciation rules? Is the asset cost under $20,000 GST-exclusive? Was the asset actually in use or installed ready for use before 30 June 2026? And if it is a vehicle, is it a passenger vehicle or a commercial one? Getting the answers to those four questions before the claim is processed prevents the most common errors and means the client's deduction is defensible if the ATO ever asks about it.