How the EDP Rules Work and Why They Create Confusion

Since 2017, international businesses selling digital products and services to Australian customers have been required to register for GST in Australia once their sales to Australian consumers exceed $75,000 per year. This covers the major platforms most clients use daily. Platforms like Adobe, Google, Microsoft, and Atlassian are registered and charge GST on supplies to Australian consumers at checkout. When a GST-registered Australian business provides its ABN and confirms it is registered for GST, many of these platforms will remove the GST charge from the invoice, because the supply is now treated as a business-to-business transaction rather than a consumer supply.

The electronic distribution platform rules determine who is responsible for collecting and remitting that GST. Where an overseas supplier sells through an EDP, the platform operator is responsible for collecting and remitting GST to the ATO rather than the underlying supplier. This is why the Apple App Store, Google Play, and similar marketplaces handle GST collection on behalf of the developers selling through them. It also means the overseas supplier does not have an ABN, because businesses registered under Australia's simplified GST system for non-residents are issued an ATO Reference Number instead. Without an ABN, the supplier cannot issue a valid tax invoice and the Australian business purchasing through that supplier may not be able to claim an input tax credit in the standard way.

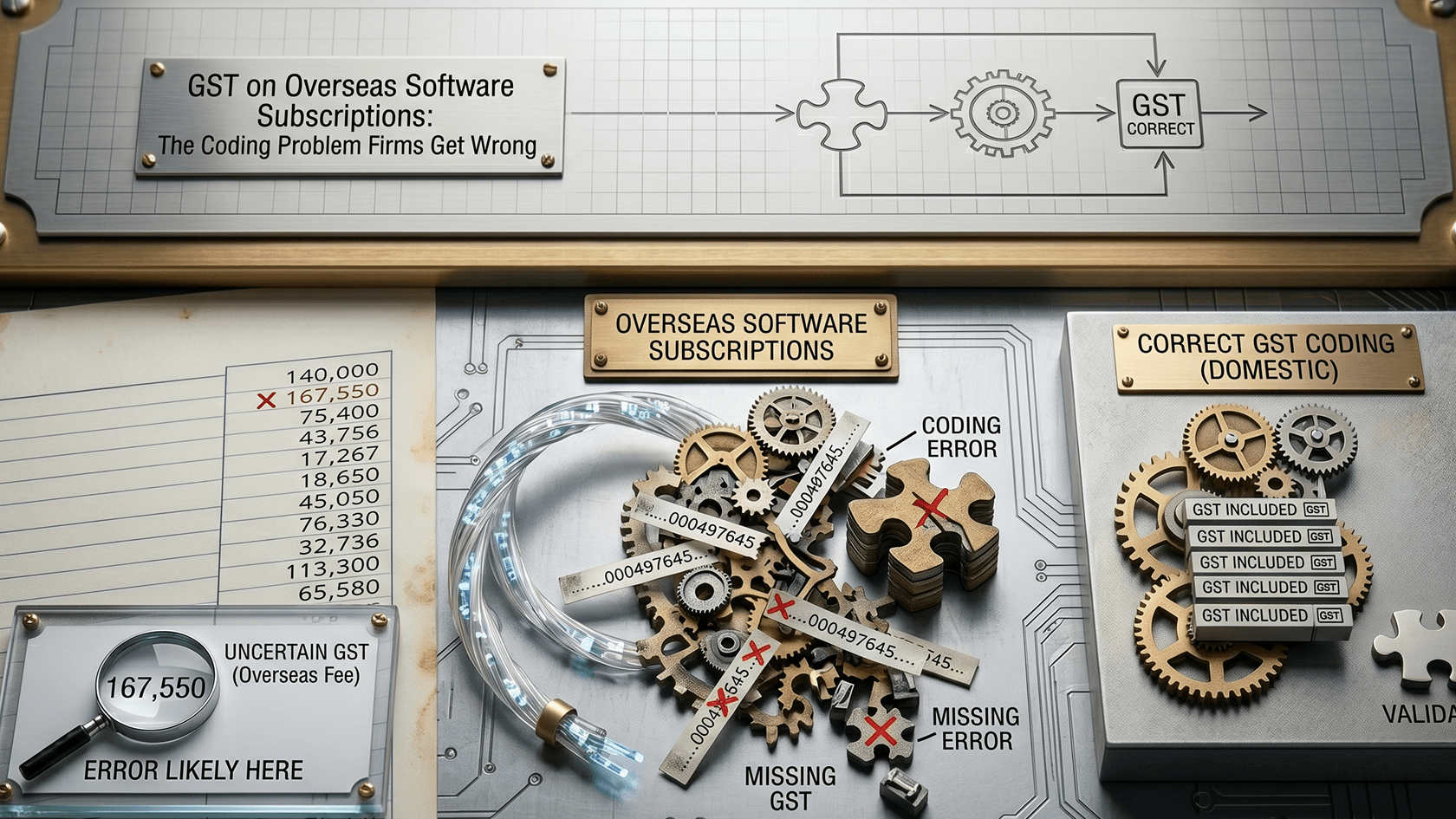

The coding problem in practice is that most bookkeepers see an overseas subscription invoice, note that there is no ABN, and code the expense as GST-free. That is wrong in a specific set of circumstances, and the right treatment depends entirely on whether GST was actually charged on the invoice and whether the business has provided its ABN to the supplier.

The Two Directions the Error Goes

The first error is coding a subscription as GST-free when the supplier has already charged and remitted GST on the transaction. If a client's Adobe or Microsoft subscription invoice shows a 10% GST component, the purchase is taxable and a GST credit can be claimed on the BAS, even though the supplier does not hold an ABN. The ATO specifically allows this where the supplier has charged GST incorrectly on a business customer but has still remitted that GST to the ATO, and where the business would otherwise be entitled to the credit. Coding the expense as GST-free in that situation means the firm is leaving a legitimate credit on the table every single quarter.

The second error runs the other way. When a supplier has not charged GST because the client correctly provided an ABN and was removed from the consumer-side collection, the reverse charge mechanism may apply. Under reverse charge rules, the Australian GST-registered business is required to self-assess 10% GST on the value of the imported service, report it on the BAS as GST on purchases, and then claim it back as an input tax credit in the same period. The net GST outcome is usually zero, but the obligation to report it exists. Firms that simply code the subscription as a clean expense with no GST treatment and no reverse charge reporting are not compliant, even though the financial impact looks neutral.

The practical audit check for existing client files is straightforward. Pull the list of regular overseas software subscriptions the client pays. For each one, check whether the invoice shows a GST component. If it does, confirm a credit is being claimed. If it does not, confirm whether the client has provided their ABN to that supplier and whether the reverse charge has been reported on the BAS. Any subscription that has been coded as GST-free without that check having been done is a potential error.

The Takeaway

The GST treatment of overseas software subscriptions is not as simple as checking whether the supplier has an ABN. It depends on whether GST was charged, whether the client is registered for GST, whether the ABN was provided to the supplier, and whether the reverse charge applies. Firms that code every overseas subscription as GST-free are likely leaving credits unclaimed for clients who paid GST at checkout, and potentially missing reverse charge obligations for those who did not. Running a quarterly check across active overseas software expenses before BAS lodgement, and verifying the treatment against the actual invoice, takes about twenty minutes per client and prevents an error that compounds silently across every period it goes uncorrected.