How the 4-Year Rule Actually Works

GST input tax credits do not stay claimable indefinitely. Under Division 93 of the GST Act, and clarified further in the ATO's Miscellaneous Taxation Ruling MT 2024/1 published in 2024, a credit expires 4 years from the due date of the original BAS for the tax period in which the credit could first have been claimed. Not 4 years from when the invoice was issued, and not 4 years from when the BAS was actually lodged. It is 4 years from the date it was due.

As an example: a client purchases equipment in March 2020. Their quarterly BAS for that period is due 28 April 2020. The 4-year credit time limit expires at the end of 28 April 2024. If that credit has not been included in an assessed BAS by that date, it is gone. The ATO has confirmed it has no discretion to extend the period or amend an assessment to include credits after the window has closed. No exceptions for administrative delays, change of accountant, or oversight.

There is also a critical process point that firms get wrong under pressure. Lodging an amendment request or voluntary disclosure does not preserve the credit. The ATO must actually process the amendment and include it in the assessment within the 4-year window. If an amendment request is sitting in the ATO's queue and the deadline passes before it is processed, the credit expires regardless. The ATO's own guidance recommends lodging a Revised BAS through Online Services rather than a written amendment request, as RBAS requests are processed faster. If credits are within one month of expiring and the amendment is still unprocessed, the ATO advises calling 13 28 66 to follow up directly.

Where This Catches Firms During Catch-Up Work

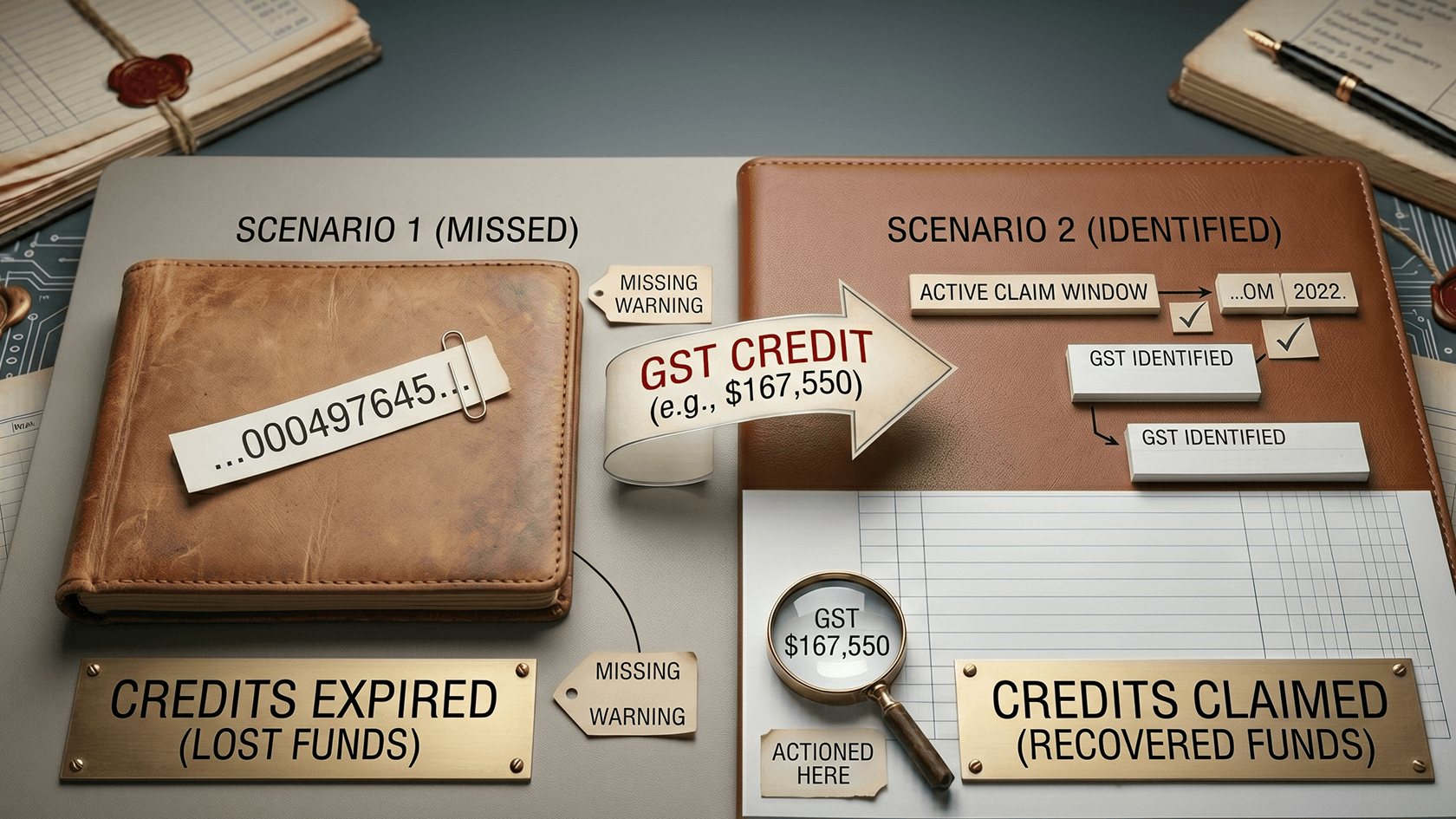

Catch-up bookkeeping is where this rule causes the most damage. A client who has not lodged correctly for three or four years arrives at the firm with a backlog of unclaimed credits. Some of those credits are still within the 4-year window. Some are not. The firm's job is to work out exactly which periods are still claimable before doing any of the catch-up work, because time spent on an expired period is time spent recovering nothing.

The calculation is straightforward in theory. Take the due date of the original BAS for each unclaimed period and add 4 years. Any period where that date has already passed is unrecoverable. What makes it complicated in practice is that clients with irregular lodgement histories sometimes have extended review periods from prior ATO amendments, or periods where the BAS was lodged late, which shifts the starting point of the review period but not necessarily the credit time limit. The credit limit runs from the due date regardless of when the BAS was actually lodged.

There is also an asymmetry worth making clear to clients. The 4-year expiry applies only to credits. There is no corresponding expiry on GST liabilities. The ATO can still assess and collect underpaid GST from those same old periods. A client with expired credits and outstanding GST liabilities from the same quarter ends up in the worst of both positions.

The Takeaway

The 4-year credit time limit is one of the few areas of tax law where there is genuinely no safety net. The ATO has been explicit: once the window closes, it cannot help. For firms doing catch-up work, the first task before touching any historical period is to calculate which credits are still within time and prioritise those. For ongoing clients, a quarterly check that no claimable credits are approaching the 4-year mark is a simple addition to the BAS preparation process that costs nothing and prevents an unrecoverable loss.