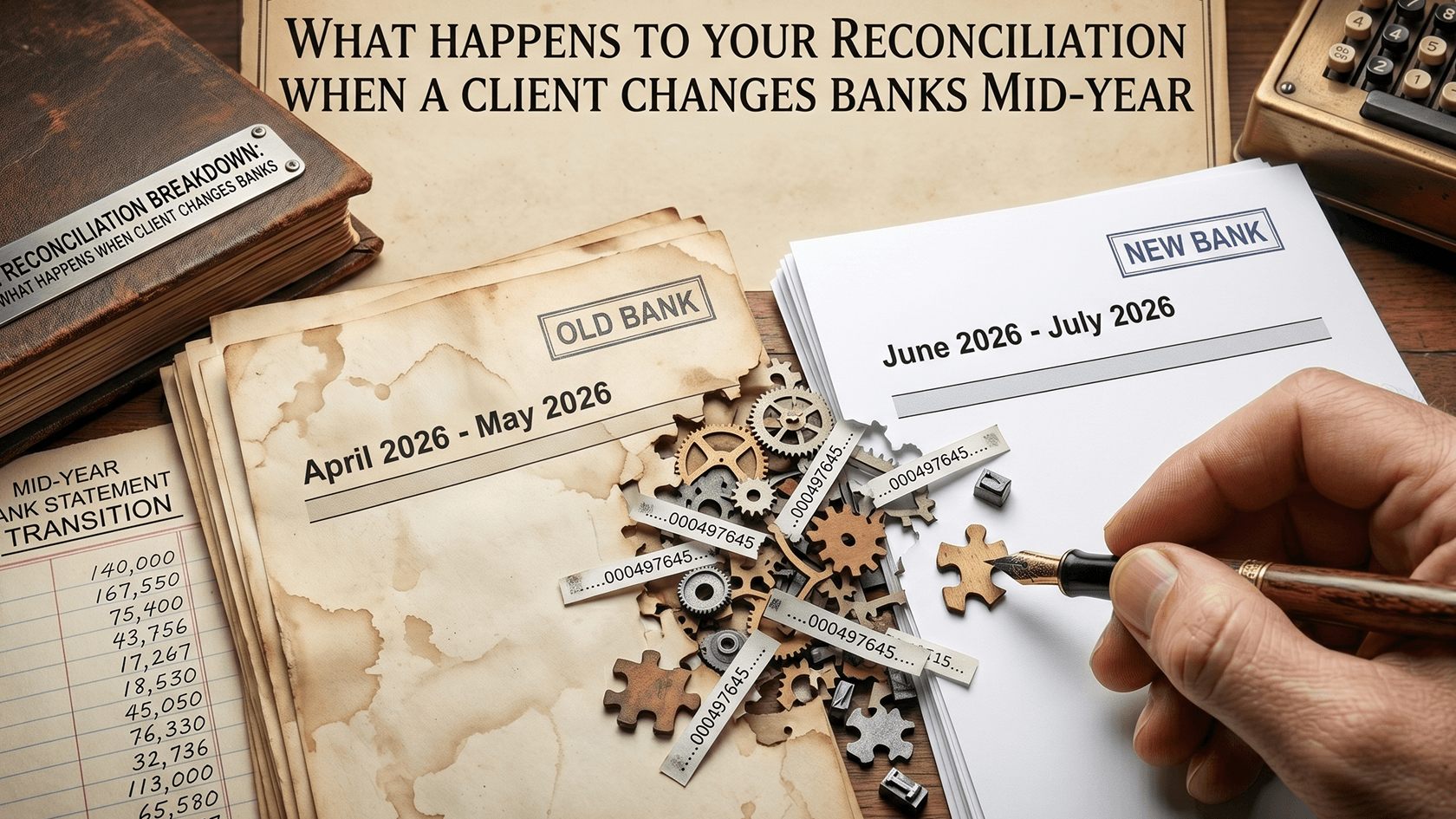

Why a Bank Switch Is a Reconciliation Event, Not Just an Admin Task

When a client tells you they have moved to a new bank, the instinct is to treat it as a straightforward update. Disconnect the old feed, connect the new one, carry on. The problem is that the period around the cutover almost always produces errors that are not obvious until the reconciliation does not balance, and by that point the cause is a few weeks in the past and harder to trace.

The first issue is the overlap period. Most clients do not close their old account the day they open the new one. There is usually a window of days or weeks where both accounts are active, payments are still arriving into the old account, and direct debits are being moved across one by one. During this period, transactions from both accounts need to be captured and coded correctly. If the firm is not aware the overlap is happening, it is easy to miss income that arrived in the old account after the team assumed the feed was no longer relevant, or to double-count a payment that cleared both accounts during the transition.

The second issue is the opening balance on the new account in the accounting software. When a new bank account is added in Xero or MYOB, the opening balance needs to reflect the actual opening balance on the bank statement at the date the account became active in the system. If that figure is set incorrectly, every reconciliation from that point forward will be off by the same amount. The error does not grow, but it also does not go away, and it will sit there causing a false variance until someone goes back and fixes the opening balance at source.

Where Duplicate Transactions Come From

Duplicates are the most common technical problem that comes out of a bank feed cutover. When a new feed is connected and historical transactions are imported to cover the transition period, there is a real risk of the same transactions appearing twice. This happens most often when the firm manually imports a statement to fill a gap in the feed history, and the feed itself then backfills some or all of the same period once it is properly connected.

Xero has a built-in duplicate detection warning but it is not reliable when the description or date on a transaction differs slightly between the feed version and the imported version. Two lines for the same transaction with a one-day date difference will both appear in the reconciliation screen without a warning. Clicking through to match both against the same invoice or payment creates a double-entry that the balance will carry silently until someone investigates an unexplained variance.

The cleanest way to handle the cutover is to establish a hard date, the date the old account was closed or the last transaction that cleared it, and import or reconcile each account only up to and from that date respectively. Any manual import to cover the gap should be done before the feed is connected for that period, not after, to avoid the overlap that produces duplicates.

The Takeaway

A client switching banks is not a set-and-forget update to the accounting software. It requires a defined cutover date, a check on both accounts during the overlap period, a correctly set opening balance on the new account, and a deliberate process for handling any manual imports before the new feed is connected. Firms that treat it as a workflow event rather than a quick admin task catch the duplicate and balance errors before they compound across the following quarter. The ones that do not will find the discrepancy eventually, but it will take longer to fix than it would have taken to handle the transition properly.