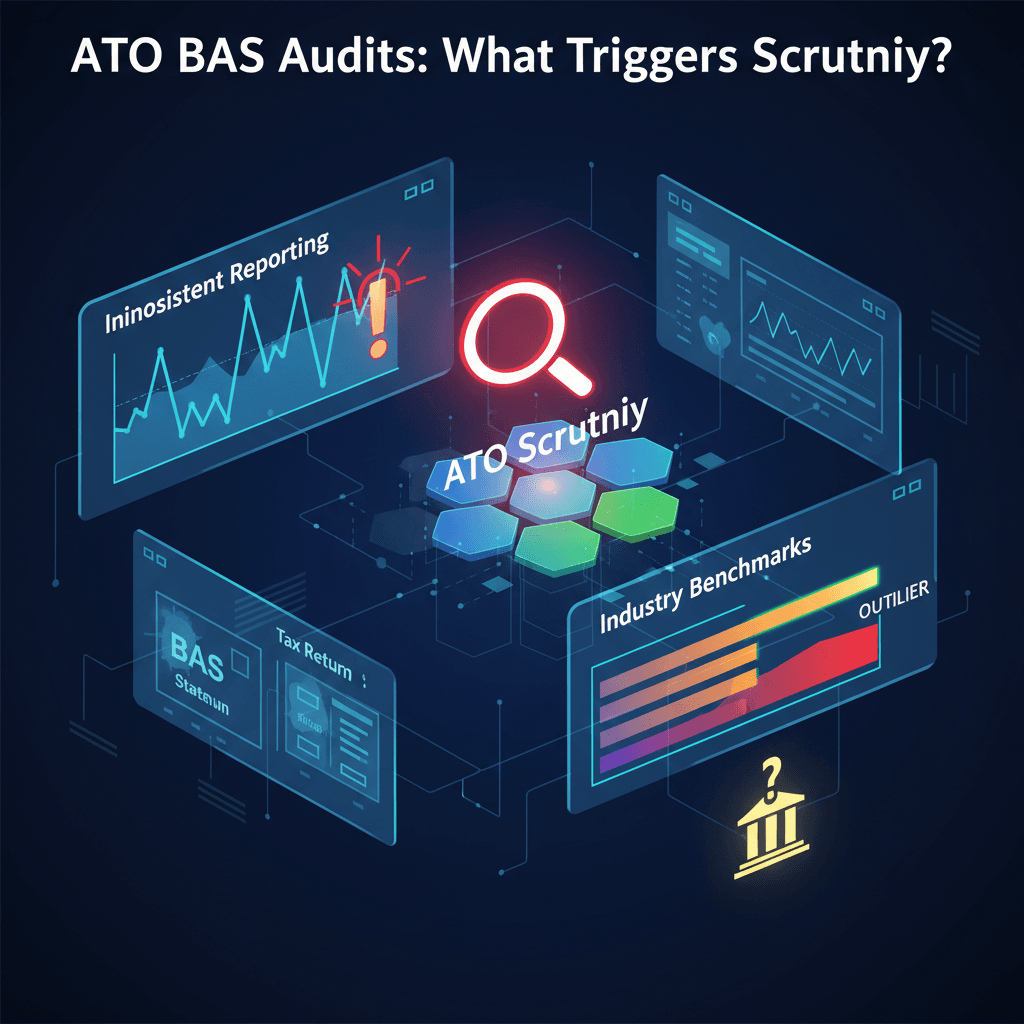

What Usually Sets It Off

When someone searches “ATO BAS audit triggers” or “why did I get a BAS review,” they’re usually trying to understand whether something specific caused it. In most cases, ATO scrutiny isn’t random. It’s pattern-based.

The ATO uses data matching across GST reporting, PAYG withholding, income tax returns, and industry benchmarks. If BAS figures move in ways that don’t align with prior reporting or industry averages, that can attract attention.

This doesn’t mean every variation causes an audit. But repeated or unusual patterns are what typically trigger review activity.

Where Risk Builds

One common trigger is significant fluctuations in GST on sales or GST on purchases without a clear business reason. If one quarter shows a sharp increase or decrease compared to previous periods, it can raise questions.

Repeated BAS amendments are another red flag. Occasional corrections are normal. Consistent revisions across multiple quarters suggest underlying process issues.

Fuel tax credits, GST on imports, and private use adjustments also attract scrutiny when claimed inconsistently. If credits appear unusually high relative to turnover, or if adjustments vary widely without explanation, that can prompt review.

Duplicate transactions from CSV imports, misclassified director loans, and GST coding drift over time can also distort BAS figures in ways that don’t match income tax reporting.

The ATO is looking for mismatches and inconsistencies, not perfection.

The Takeaway

ATO BAS audits are usually triggered by patterns, not isolated mistakes. Keep GST coding consistent, avoid repeated amendments without resolving root causes, and ensure large movements in BAS figures are documented and explainable.

When transaction-level data is clean and supported by proper records, scrutiny becomes far less stressful. Most reviews aren’t about one number. They’re about whether your reporting makes sense over time.